The history of government borrowing in Finland goes back almost 200 years. During this period, Finland has overcome economic difficulties on several occasions and retained its credibility as an issuer, which has supported economic development. President Sauli Niinistö took over the role of Minister of Finance in 1996 in the aftermath of a deep recession and several years of unprecedented growth in government debt. “And yet there was a belief that we would get through this – as, in time, we did. The mood in Finland was that the job simply had to be done.”

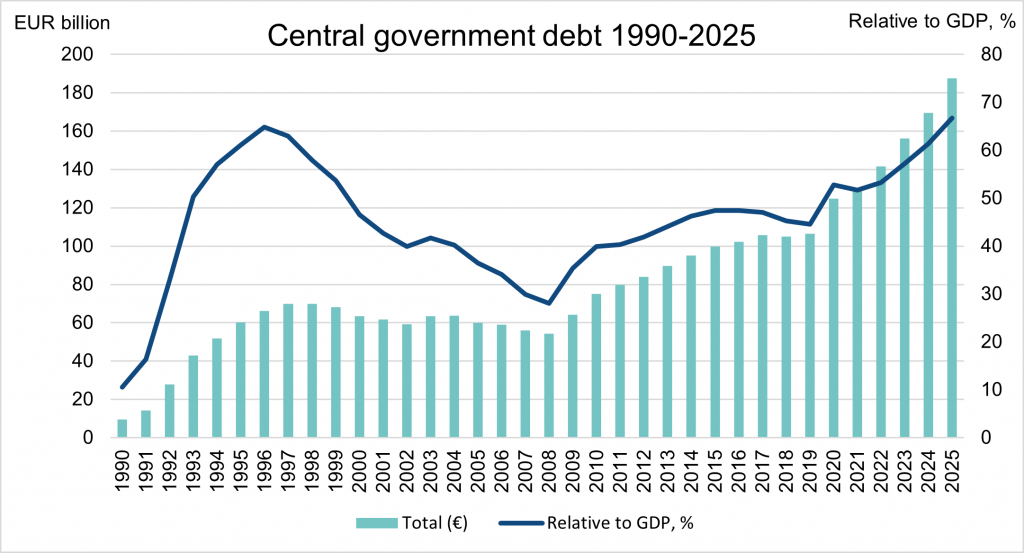

The central government was nearly debt‑free in the late 1980s, until the recession of the 1990s changed everything. The Finnish economy and central government finances were hit by a deep crisis, which resulted in a sharp increase in government borrowing. Much has been written about the causes and events of the 1990s recession – and about how close Finland came to a point where investor confidence in the government’s ability to service its debt might have been lost. In any case, the debt‑to‑GDP ratio went up from just over ten percent to roughly 65 percent in only six years (1990–1996).

Today’s figures look much the same. At the end of 2025, Finland’s estimated central government debt‑to‑GDP ratio stood at 67 percent.

Finland’s debt-to-GDP ratio was in 1996 at roughly the same level as it is in 2025. Source: treasuryfinland.fi

Sauli Niinistö assumed the role of Minister of Finance in Prime Minister Paavo Lipponen’s first government at a time when the worst of the recession had passed and the economy had begun to recover. Even so, substantial spending cuts were still required to balance central government finances, on top of those already implemented by the previous government led by Prime Minister Esko Aho.

“The 1995 Budget was drafted so that nearly one third of it was financed by debt. This did not materialise in the final accounts, as growth had already resumed and the worst had passed. But the starting point was rather extraordinary even compared with today’s borrowing – in relative terms, I mean,” President Niinistö says.

“I hope I’m remembering correctly, but that’s the figure I have in mind.”

Sauli Niinistö was the last Finnish Minister of Finance to travel the world to meet international investors to facilitate government borrowing. His first term as Finance Minister, from 1996 to 1999, coincided with a pivotal transition period: Finland had recently joined the European Union and was moving toward adopting the common currency. Meeting the criteria for entry into the euro area became a key driver of economic policy for a country still recovering from recession.

But during those same years, the Finnish economy also began to grow at an unprecedented rate. Later on in the euro era, senior government figures were no longer needed to lend credibility to investor meetings. Confidence in Finland on the financial markets strengthened regardless.

“[Iiro] Viinanen had toured Japan, and as I recall, those visits were among the most important. I also went on a roadshow there in 1996, which turned out to be much easier than I had expected. The Japanese bankers viewed us surprisingly favourably. They knew the stories of a country that pays its debts,” Niinistö recalls of his early days in office.

Boosted by strong economic growth, Finland quickly met the Maastricht criteria for joining the euro area in the latter half of the 1990s – including price stability and sound public finances. According to Niinistö, this was transformative.

“When it began to look almost certain – also in the eyes of lenders – that Finland would join the euro area, it actually changed everything. And of course, our general government figures also started to improve dramatically.”

Finance Minister Sauli Niinistö waits in the government gallery in September 1996 for fellow ministers to arrive before presenting the next year’s budget proposal to Parliament. Niinistö had taken office earlier that year. Photo: Lehtikuva / Markku Ulander

Finland’s debt‑to‑GDP ratio fell faster than in any other country between 1996 and 2001 – by more than 25 percentage points. By 2001, the ratio had dropped to below 40 percent.

A country without problems

The expectation of euro‑area membership, together with a strengthening economy, was also reflected in Finland’s bond yields, which gradually converged with those of Germany. Anu Sammallahti, now Head of Debt Management at the State Treasury, worked in fixed-income trading at Kansallis‑Osake‑Pankki – later merged into Nordea – between 1994 and 2000.

“From an investor’s standpoint, the visibility of a convergence path for bond yields combined with an improving fiscal outlook is an appealing mix. In such an environment, the product essentially sells itself,” Sammallahti says.

Euro adoption fundamentally changed government borrowing. When the euro was introduced as an accounting currency at the beginning of 1999, the issuance shifted to a new playing field: the euro area bond market, then the second largest in the world after the US dollar market. Finland converted its markka‑denominated bonds into euros already at this stage, supporting good market liquidity from the outset.

In 2001, Sammallahti joined the State Treasury, which had taken over all government borrowing from the Ministry of Finance a few years earlier. The adoption of the euro meant that the investor base for central government debt became almost entirely international within a few years. It also reshaped risk management: currency risk vanished, and the euro‑denominated interest rate swap market presented new possibilities for managing interest rate exposure

“In those days, the concerns of government debt managers centred on secondary market liquidity at a time when Finland’s national debt was expected to decline,” she recalls.

At the State Treasury’s front office, market developments are monitored at close range. The photo is from 2015, when Anu Sammallahti headed the unit responsible for government funding, liquidity management and investor relations. Photo: Lauri Rotko

The turn of the millennium was a good time for Finland and Finland’s central government finances in every way. Finland’s credit rating was back to the top AAA rating in 2002, a year in which the general government surplus was one of the highest in the euro area. Thanks to the strong economic development driven by Nokia, Finland’s bond yields were at par with those of the German government – and even lower occasionally.

Were the years 1999–2003 perhaps happier times for the Minister of Finance as well?

“I’ve sometimes said that as long as times are tough, the Minister of Finance has an easy job. During Prime Minister Lipponen’s second government, Nokia’s stock options dominated the headlines. People began to think there must be a hell of a lot of money somewhere. The atmosphere changed rather quickly, as up until then safeguarding the central government’s finances had somehow been a shared concern,” Sauli Niinistö says.

“Democracy reflects the public mood,” Niinistö points out. After the severe spending cuts, many people were dismayed by the constant media coverage of Nokia’s stock option millionaires. According to Niinistö, this contributed to a widespread view in economic policy debate that it was now time to loosen the purse strings.

“This is why I don’t think much of my final years as Minister of Finance. It was a desperate defence battle.”

A troubled relationship

Debt and indebtedness make many of us uncomfortable. Surveys show that Finns worry about the rising central government debt. We take debt sustainability seriously – so seriously that proposing spending cuts can open doors to political success in Finland.

Professor Emeritus Sakari Heikkinen suggested in Helsingin Sanomat (Velkapeikon vangit, 28 December 2025, in Finnish only) that Finns’ fear of debt stems from our history. In Finland, borrowing and debt management have been viewed as part of building the young nation’s reputation, which required the country to act as a model pupil. The threat posed by the Soviet Union affected government borrowing for a long time, and instead of having a casula relationship to it, Finns respected and dreaded borrowing.

In Finland, credibility in financial markets has long been seen as essential to government borrowing. This is evident in the prominent role senior political leaders have played in securing funding – from J.V. Snellman, J.K. Paasikivi and Risto Ryti to Esko Aho, Iiro Viinanen and Sauli Niinistö.

In the world’s happiest country, people’s dreams tend to be realistic – and often connected to debt. More than our Nordic neighbours, Finns dream of paying off what they owe as quickly as possible. Both Niinistö and Sammallahti point to the pursuit of economic independence as a key factor in shaping Finns’ attitude toward debt.

A third explanation, which Heikkinen also highlighted, is the association between rapidly rising debt levels and times of crisis. In particular, the painful experiences of the 1990s recession left deep scars.

“Once things get serious, Finns will deliver”

What are we facing now? For more than a century, Finland followed a tradition of prudent management of public finances, with the view that borrowing was justified only when it supported economic strength. That tradition has not held since 2008 – and even less so in the 2020s. Current estimate is that 14% of the 2026 Budget will be financed by borrowing.

“The big question is whether Finland’s indebtedness over the past 17 years has been driven by maintaining the standard of living we’ve grown accustomed to. If we begin funding our consumption with other people’s money – and grow comfortable with it – how much does that take our focus away from the progress we should be making ourselves?” Niinistö asks.

Niinistö sees mental parallels between the late 1980s boom and the era of negative interest rates.

“At the end of the 1980s, people believed that foreign currency was cheap and easy to access. This time, we thought that borrowed money was cheap and easy to access. Even the media contributed to the general mood, especially early this decade: money was available, and there was little need to pay it back. These things were taken far too lightly. And in my view, this also paved the way for the current deficit,” Niinistö continues.

So did borrowing become too easy for the government? There are counter-arguments to this view: after the financial crisis, the euro area and Finland have been hit by repeated shocks that, especially in the 2020s, seem endless. As a result, countries have become indebted almost everywhere.

This is a relevant point as well, since the single currency creates a joint playing field for the eurozone countries.

“And on a joint playing field, relative performance matters as well – for example, whether our fiscal deficits are larger or smaller than those of others, or what is our debt ratio,” Sammallahti explains.

Amid an uncertain future and the negative tone of domestic discussion on debt, it is worth remembering that Finland’s strengths have not disappeared. Although our demographic structure is no longer what it was in the mid‑1990s and global developments have not supported economic growth in the recent years, the future is not predetermined. We are not condemned to permanently low growth.

Around the world, Finland is still seen as reliable, and according to Niinistö and Sammallahti, this has not changed. In international contexts, Finns are regarded as people who keep their word rather than make empty promises.

“Those who take things seriously, will be taken seriously. And being boring is a good selling point in the bond market,” says Sammallahti.

Niinistö points out that there is no ranking of positive things in the world – be it happiness, lack of corruption or freedom of the press – where Finland would not take the podium or at least a high rank.

When reflecting on Finland’s future, the former Minister of Finance is reminded of Joseph Schumpeter’s theory of creative destruction – albeit in a slightly adapted form. When things get bad enough, he says, a shared realisation finally emerges: something has to change.

“Calling it creative chaos may be a bit rough, but I trust that as things become more serious, Finns will turn a corner and face their problems”, he says.

After all, that’s what we’ve done it before.

Text: Tiina Heinilä

Cover photo: Henni Purtonen

This article draws on Mika Arola and Sakari Heikkinen’s work on the global history of Finland’s government borrowing, Hyvä, paha valtionvelka – valtion lainanoton globaali historia (Gaudeamus, 2025).

Sauli Niinistö is Finland’s longest‑serving Minister of Finance (1996–2003). After his ministerial years, Niinistö served as Vice‑President of the European Investment Bank (EIB) in Luxembourg from 2003 to 2007, as Speaker of the Finnish Parliament from 2007 to 2011, and completed two terms as President of the Republic of Finland from 2012 to 2024.

Anu Sammallahti is responsible for government debt management at the State Treasury of Finland. She has held senior positions in government funding, liquidity management and investor relations since 2010, and has headed the Debt Management Department since 2025.